Was this newsletter forwarded to you? Sign up to get it in your inbox every week

Last Tuesday, I watched a $4M software startup implode in exactly 72 hours. Their product? Brilliant. Their team? Top-tier. Their bank account? Empty.

Here's the thing about business storms: They don't ask for permission. They don't check your calendar. They just show up - like that relative who crashes on your couch "just for a weekend" and stays for a month.

But while we can't control the weather, we can build one hell of an umbrella.

This week's playbook is your storm-proofing guide:

Building a cash reserve → Because running out of money is scarier than any horror movie

Setting up a BCP → Your business's survival guide when things go sideways

Cost-cutting audits → Finding hidden money leaks before they sink your ship

Think of this as your business's insurance policy - except instead of putting you to sleep, it might just save your company.

P.S. No one wants to build solo. Let’s connect

Want to co-build something?

Thousands of you have asked for executive coaching. I've been listening. And thinking. And pondering. And I think I’ve got an answer.

I got something cooking…

If you want to help, just click on the button below. I’ll email you to schedule time to jam on a call.

How much money should your business keep in reserve? (Factor This)

Your free business continuity template here (Pipedrive)

Get a free business cost saving audit template (Zapier)

6 ways to manage your cashflow (NerdWallet)

Apple almost went bankrupt in the 90’s… How? (TheStreet)

I. Cost-Cutting Audits

Insight from HBR.

When it comes to cost-cutting, businesses often fall into the trap of trimming the obvious like fewer office snacks or skipping that big conference.

But a real cost-cutting audit is about digging deeper into your spending, finding areas where dollars are slipping through the cracks, and putting those dollars back where they belong (hint: not the snack budget).

Here’s a quick checklist of things to audit when times get tough:

1. Software Subscriptions

It’s shocking how many tools we sign up for without fully using them. Companies often pick up software left and right, justifying each purchase as “only $30 a month” – until it’s ten subscriptions later, and that budget line’s ballooned.

Chances are, you’ve got overlapping features – like two different tools doing 90% of the same things.

Try to list every software you pay for monthly, list their features, and identify any overlap. If you’re only using 30% of a tool, consider saying goodbye to it.

2. Marketing

Many businesses throw money at ad campaigns, cross their fingers, and hope for magic. But without a roadmap that guides leads from the ad click to the purchase, you’re basically throwing cash into the wind.

First, outline your marketing strategy, mapping out each step from lead generation to conversion. If you can't directly link a tactic to conversions, consider cutting it or finding a more strategic use of that budget.

3. Taxes

Ever had your accountant tell you after the fact that you could’ve saved money with a different tax strategy?

That’s a missed opportunity – and it happens too often. Instead of meeting with your accountant at the last minute, schedule regular check-ins to discuss current tax-saving opportunities throughout the year.

Proactive tax planning can help you lock in deductions or credits that would otherwise slip by.

4. Payroll

Here’s a common trap: hiring ‘middle’ talent. It’s not that the mid-level hires aren’t great, but you may be paying a higher salary for tasks that could’ve been handled by more junior talent – or by a specialist for a few hours.

The trick is to assess the exact skill level needed for each task and to allocate hours wisely. With today’s gig economy, you can cherry-pick the expertise you need without paying full-time salaries across the board.

Why not try to identify specific tasks that can be outsourced at different levels, such as entry-level, mid-level, and expert? Then you can seek talent accordingly.

Cost cutting is about running a leaner, smarter business. By auditing these things above, you’ll have more resources left to actually grow your business – rather than keeping up with unnecessary expenses.

Now, if only you could convince the team to skip those daily $5 lattes...

II. Building a cash reserve

Insight from The Kenza Pod

Every business needs a cash reserve. Not just because it sounds financially responsible, but because life is full of “Oops, didn’t see that coming” moments.

You don’t want to end up scrambling for funds when the next crisis hits, like your main supplier going rogue or your trusty laptop suddenly deciding it’s nap time—for good.

Let’s get into a solid, but not-too-serious, strategy to set up a cash reserve that’s ready to bail you out, whatever the surprise.

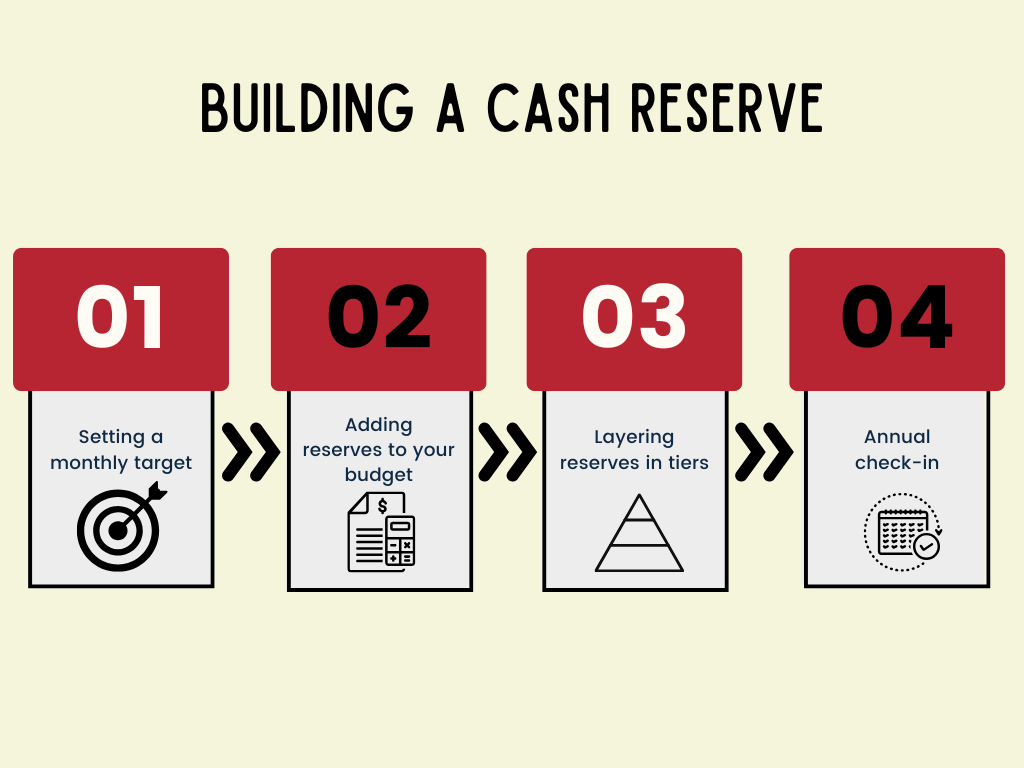

Step 1: Set a Monthly Target and Hit Autopilot

It’s recommended to have at least 3-6 months worth of your operating expenses as a cash reserve.

Trying to save that pile of money all at once? Not fun. Instead, break it down into monthly chunks and let automation do the work. This way, saving feels like less of a chore and more like a routine.

Look at your monthly revenue and decide on a percentage you can live with. Most businesses aim for 5-10%. If that sounds ambitious, start smaller and work your way up.

Next, set up a recurring transfer from your main account to a dedicated reserve fund each month. The key here is consistency, not huge amounts—let automation be your savings buddy so you don’t have to think about it every month.

Say you bring in $20,000 a month and decide to sock away 5%. That’s a simple $1,000 each month, which adds up fast without making you feel like you’re giving up all your profits.

Step 2: Add it to the Budget (No, Really, Make it Non-Negotiable)

The best way to actually stick to this plan? Treat your cash reserve like a fixed monthly expense. Yup, just like payroll or that monthly coffee subscription nobody remembers signing up for. By making it a priority in your budget, it becomes a habit—and habits are harder to skip.

Step 3: Layer Your Reserve in Tiers

This is where things get interesting (and slightly fancy). Instead of dumping everything into one account, create a layered reserve based on how quickly you might need access to it.

A tiered system gives you flexibility—and maybe a bit of interest income—while keeping emergency funds accessible.

Tier 1: Cold Hard Cash – Keep one or two months of expenses in an easy-to-access savings account.

Tier 2: High-yield Savings or Money Market Fund – Another two to three months here, where it’s earning a bit of interest but still easy to grab if you need it.

Tier 3: Short-term CDs or Treasury Bills – This is where you can put funds you’re not planning to touch soon. Still accessible, but with a bit more growth potential.

Having this setup is like bringing both a raincoat and an umbrella—you’re prepared no matter the situation.

Step 4: Annual Check-In (A Little Business Health Assessment)

Businesses evolve, so your reserve should, too. Once a year, give your cash reserve a check-up. Look at your expenses, future plans, and any major business changes to see if you need to tweak your reserve goals.

If you’re anticipating a big expansion or a new hire spree, bulk up that reserve ahead of time. Think of it as prepping for the future, not just reacting to the present.

This keeps your reserve plan nimble and makes sure it’s up to date with the realities of your business.

With a bit of planning, discipline, and the right strategies, building a business cash reserve can be one of the best moves for your peace of mind and your business’s future.

III. Setting up a BCP

Insight from HR Party of One.

In simple terms, BCP is the game plan that keeps business operations humming along during a disaster. Whether it’s a power outage, system failure, or something as drastic as an earthquake, BCP ensures that business interruptions are kept to a minimum.

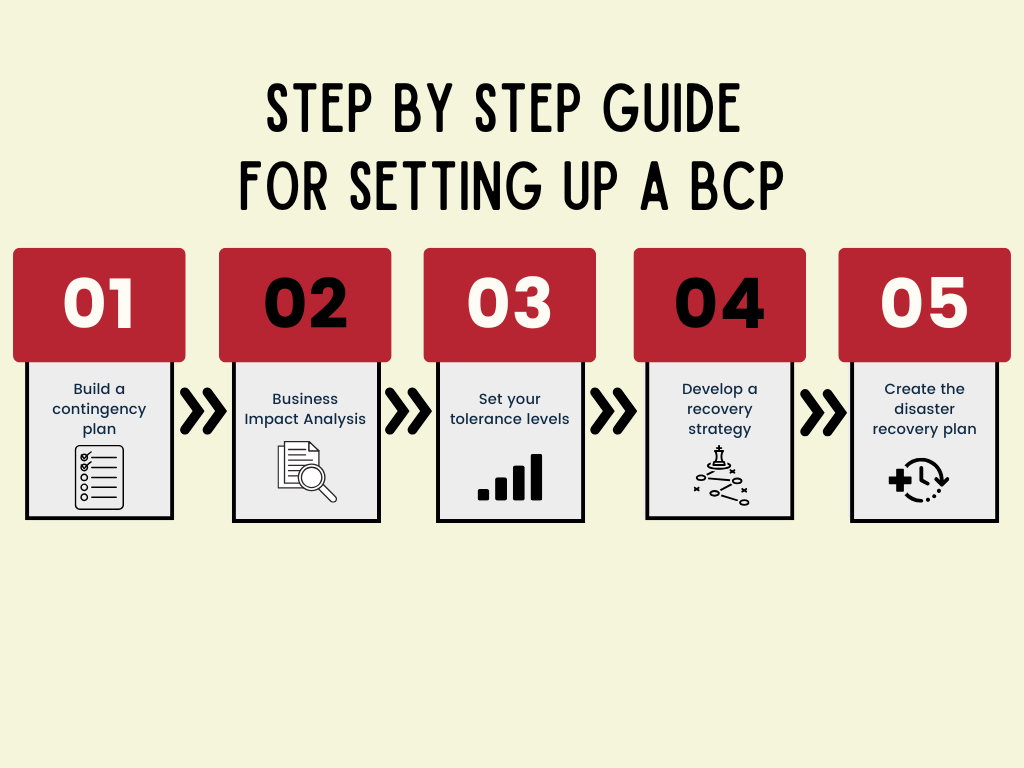

Let’s break down some actionable steps for building a rock-solid BCP.

Step 1: Build a Contingency Policy

Start with the basics. You need a contingency policy—this is the rulebook everyone in the organization will follow in a crisis. Make sure top management is involved, and get their statements of support, which can also set boundaries like which regions the plan applies to.

This policy is the framework that lets everyone know you’re serious about keeping things running no matter what.

Step 2: Business Impact Analysis (BIA)

The BIA is all about figuring out what’s mission-critical and what can wait. It’s like a triage system—you’re deciding which services and assets absolutely cannot go down and for how long they can stay offline before the costs become painful.

Here’s the BIA Process:

List all business processes: Identify your revenue-generating processes and who owns them.

Estimate the revenue impact: Calculate the potential losses if each process goes down.

Set up meetings with key players: Understand the importance of each process directly from the business owners.

Prioritize based on impact: Decide which processes to recover first, like who needs a hot site (instant switch-over) and who can make do with a warm site (recovery within a few hours).

Step 3: Set Your Tolerance Levels (MTD, RTO)

Once you know the critical processes, you’ll need to pin down Maximum Tolerable Downtime (MTD) and Recovery Time Objectives (RTO) for each one.

MTD is the absolute maximum time a service can be down without causing major issues.

RTO is how quickly you aim to recover each service. Say your MTD for a process is 30 minutes; your RTO should be something achievable within that timeframe, like 25 minutes.

Step 4: Develop a Recovery Strategy

Now you’ve got to create a recovery strategy based on the BIA findings and tolerance levels. This is where you make the big decisions:

Which sites or servers will be redundant?

Who gets priority if two services are down at once?

What’s the backup plan for power or internet failures?

Present alternative solutions too! Sometimes, a full backup server might be overkill. Offer a more cost-effective option like cloud storage or data redundancy that could bring down the costs significantly.

Step 5: Create the Disaster Recovery Plan (DRP)

Now it’s time to roll up your sleeves and outline a Disaster Recovery Plan (DRP), detailing how you’ll recover specific processes and services. The DRP should include:

Contact information for critical personnel,

Step-by-step actions to restore services,

Target times for recovery.

Test the DRP regularly and keep it updated so it’s ready when disaster strikes. The goal is to make switching from one site to another—like from your primary server in Noida to the backup in Gurgaon—a smooth, near-instantaneous process.

Help me help you

Spread The Word

If you learned something today, I’d appreciate you forwarding this to a friend. It’ll take you 2 seconds. It took us 17 hours to write today’s edition.